Active vs Passive Investing: Which Approach Actually Wins?

Written by

Published On

May 4, 2026

March 12, 2026

10 min read

Table of Content

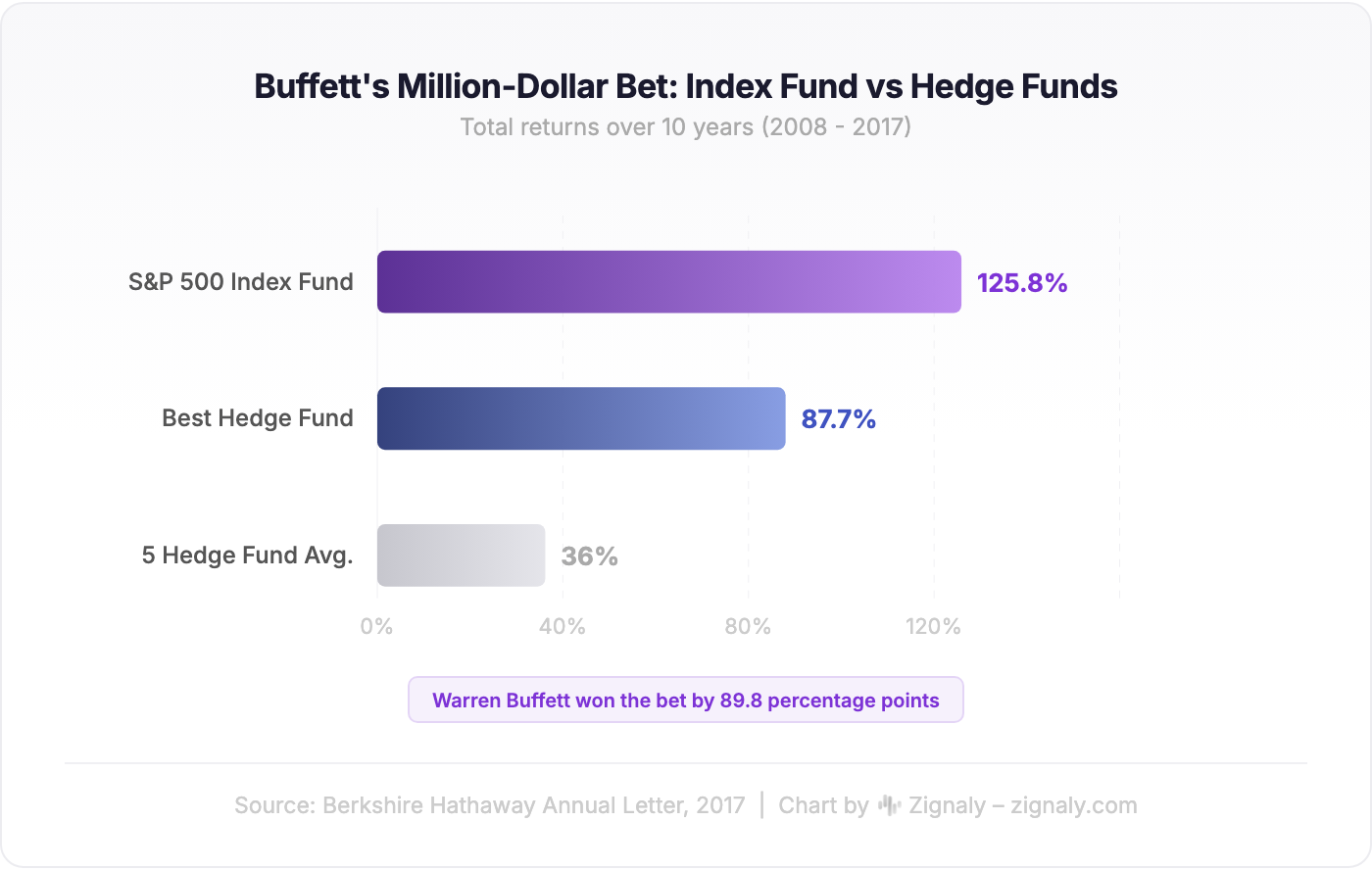

In 2007, Warren Buffett made a million-dollar bet against one of the most respected hedge fund selection firms in the world. The wager was simple: a Vanguard S&P 500 index fund would outperform a hand-picked portfolio of five hedge funds over the next decade. Protege Partners, who took the other side, had every incentive and resource to pick winners. By 2017, Buffett's index fund had returned 125.8%. The best hedge fund in Protege's basket managed 87.7%. The average across all five came in at 36%.

I remember reading about this bet years ago and thinking it was almost too clean to be real. A billionaire proving that doing less beats doing more? But the more I looked at the data behind it, the more I realized the Buffett bet was not an anomaly. It was a compression of something that plays out across thousands of funds, every single year.

What You'll Learn

- Why the data consistently favors passive investing over active management across almost every market and time horizon

- How fees compound against active investors in ways that are easy to underestimate until you see the math

- Where active management still has a genuine structural edge (and it is narrower than most people think)

- The behavioral gap that costs investors more than bad stock picks ever could

- How managed passive approaches solve the discipline problem without the cost burden of traditional active funds

Active Investing: Skill, Judgment, and the Cost of Both

Active investing means someone is making deliberate decisions about what to buy and sell, and when. That someone could be a professional fund manager leading a team of analysts, or it could be an individual investor doing their own research. Either way, the goal is the same: beat a benchmark. Usually the S&P 500, the FTSE 100, or whatever index represents the relevant market.

Fund managers use fundamental analysis, technical signals, macroeconomic forecasts, and sector rotation strategies to find securities they believe are mispriced. They trade frequently. They adjust their holdings based on market conditions, earnings reports, geopolitical events, and sometimes just conviction. This is expensive. Management fees range from 0.5% to over 1.5% annually, and that is before trading costs, performance fees (common in hedge funds at 20% of profits), and operational overhead.

The pitch is straightforward: you pay more because expertise should find opportunities that the broader market has missed. And honestly, that pitch is not wrong in every case. Active management has a genuine edge in certain conditions.

Small-cap stocks, emerging markets, and distressed corporate situations all feature information asymmetry that skilled managers can exploit. In fixed income, particularly high-yield and municipal bonds, active managers navigate credit risk in ways that a passive index cannot replicate efficiently. These are real advantages, not theoretical ones, and they show up in the data when you look at the right asset classes.

But here is the part that makes the whole thing complicated: even when active management works in a particular segment, you still have to identify which manager will deliver before they do it. And that identification problem turns out to be almost impossibly hard.

Passive Investing: Less Drama, Lower Costs, Same Market

Passive investing takes the opposite stance entirely. Instead of trying to beat the market, you buy the market. You hold index funds or ETFs that replicate a benchmark, and you wait.

No stock picking. No timing. No research teams.

Common passive vehicles include S&P 500 index funds (Vanguard's VOO, iShares' IVV), total stock market funds (VTI), global index funds (VWRL on the London Stock Exchange), bond index funds, and multi-asset funds that combine stocks and bonds in a single product. Is the S&P 500 itself active or passive? Neither. It is a benchmark. But funds that track it are passive investments.

The fee advantage is not subtle. A typical passive fund charges between 0.03% and 0.20% annually. A typical active fund charges 0.50% to 1.50%. That gap might look small expressed as percentages, but compound it over decades and the numbers become visceral.

Two investors start with $100,000 each. Both earn 8% gross returns over 30 years. The passive investor paying 0.10% ends up with approximately $980,000. The active investor paying 1.10% ends up with approximately $740,000. Same starting point, same market return, a $240,000 difference caused entirely by fees. Not by bad luck, not by poor stock picks. By the cost of having someone try to do better.

Fees are the one variable in investing you can control with certainty. I have changed my mind on a lot of investment opinions over the years, but this one only gets stronger the more evidence I see.

Markets are unpredictable. Costs are not.

What 20 Years of Data Actually Shows

The SPIVA Scorecard, published by S&P Dow Jones Indices, is the most comprehensive study of active vs passive fund performance available. It tracks how many actively managed funds beat their benchmark across regions, asset classes, and time periods.

The results are remarkably consistent:

- Over 1 year, roughly 60% of US large-cap active funds underperform the S&P 500

- Over 5 years, approximately 79% underperform

- Over 10 years, approximately 87% underperform

- Over 20 years, more than 90% underperform

These are not cherry-picked years or isolated markets. The pattern repeats in Europe (over 90% of euro-denominated large-cap active funds underperformed the S&P Europe 350 over 10 years), in Asia, and across most asset classes. Bull markets, bear markets, sideways markets. The data does not care about market conditions.

Three structural forces explain why this keeps happening. First, fees create a headwind. A fund charging 1.2% must outperform by at least that amount every year just to break even with a passive alternative. That is a significant handicap compounding against you indefinitely. Second, reversion to the mean works against persistence: managers who outperform in one period tend to underperform in the next, making it nearly impossible to distinguish skill from luck in the short term. Third, market efficiency in large liquid markets means information is priced in quickly, and finding consistent mispricings requires being systematically right when thousands of other professionals with the same data and tools are wrong.

If you had randomly selected an active large-cap fund in 2004, there was less than a 10% chance it would still be outperforming its benchmark 20 years later. That is not a particularly encouraging statistic for anyone trying to pick winners.

| Factor | Active Investing | Passive Investing |

|---|---|---|

| Goal | Beat the market benchmark | Match the market benchmark |

| Typical annual fees | 0.50% - 1.50%+ | 0.03% - 0.20% |

| Fund manager involvement | High (frequent decisions) | Minimal (tracks an index) |

| Trading frequency | High (turnover 50-100%+) | Low (rebalance with index changes) |

| Tax efficiency | Lower (more taxable events) | Higher (fewer distributions) |

| 20-year outperformance rate | Less than 10% of funds | Matches index by design |

| Best suited for | Niche markets, special situations | Core portfolio, long-term wealth |

| Investor time required | High (research, monitoring) | Low (periodic review) |

The Behavior Problem Nobody Talks About Enough

Most comparisons of active vs passive funds focus on fees and returns. They miss the bigger problem entirely.

Dalbar's annual study of investor behavior shows that the average equity fund investor underperforms the funds they invest in. Over the 30 years ending in 2023, the S&P 500 returned roughly 10.2% annually. The average equity fund investor earned approximately 6.8%. That 3.4% gap is not a fee problem. It is a behavior problem.

Investors buy after prices have risen. They sell after prices have fallen. They switch strategies after a bad quarter. They chase whatever performed best last year. This pattern affects everyone, but it punishes active investors disproportionately because the strategy itself demands more decisions.

More decisions mean more opportunities to make emotional mistakes.

At least in my experience watching how people actually behave with their money, the strategy you can follow without panicking during a 30% drawdown matters more than the strategy that produces the best historical backtest. A passive portfolio that an investor holds through a correction beats an active portfolio that the same investor sells at the bottom by a wide margin. And this is something that almost never shows up in the traditional active vs passive performance comparisons.

The real lesson of the Buffett bet is not that passive is smarter. It is that passive is easier to stick with. The hedge fund managers were genuinely skilled. But skill plus fees plus complexity, stacked against a strategy that required zero decisions after the initial one, lost convincingly over ten years.

Managed Passive: A Middle Ground That Actually Works

The active vs passive debate is often framed as a binary choice, which is a bit misleading. In practice, many investors benefit from something that combines elements of both.

Managed passive approaches use low-cost index funds and ETFs as building blocks (the passive part), while applying systematic rebalancing, risk management, and asset allocation adjustments (the oversight part). You get the cost advantage of passive investing with the discipline of having a professional ensure your asset allocation stays on track.

Managed portfolios that follow this model typically use index funds for their core exposure, apply rules-based rebalancing rather than market predictions, adjust allocations based on risk profiles rather than headlines, and charge substantially lower fees than traditional active management.

For time-poor professionals who want market exposure without daily monitoring, this approach solves a real problem. You are not paying for someone to try to beat the market. You are paying for someone to keep you from making the behavioral mistakes that cost the average investor over 3% per year.

Zignaly's Z-Indexes follow this principle: multi-asset managed portfolios across three risk levels, starting from $10, with a success-based fee structure where you pay 10% of profits. No management fee when returns are flat or negative. It is a structure designed for people who understand that the real cost of investing is not the fee, it is the gap between what the market returns and what you actually earn.

Where This Breaks Down

No approach is perfect, and pretending otherwise would undermine everything above. Passive investing has real limitations.

If literally everyone indexed passively, price discovery would stop functioning. Markets need active participants to set prices and allocate capital to productive uses. This is the passive investing paradox, and it is a genuine intellectual challenge to the "just index everything" argument. In practice, though, we are nowhere near the point where passive dominance would impair market function. Active trading still accounts for the vast majority of market volume.

More practically, passive investing does not protect you from yourself. A portfolio of three index funds can still be sold in a panic. Broad market declines affect passive investors fully, and the simplicity of selling everything with one click makes it dangerously easy to do the wrong thing during a downturn. That is precisely why managed approaches, which add friction and accountability, have value even when the underlying investments are entirely passive.

There is also the question of concentration risk. The S&P 500 is currently more concentrated in a handful of mega-cap technology stocks than at almost any point in history. Indexing means accepting that concentration passively. Whether that concerns you depends on your time horizon and diversification across asset classes, but it is worth understanding what you are actually buying when you buy "the market."

Conclusion

The evidence is directional and it has been consistent for decades. Most active fund managers underperform passive benchmarks over the long term, and the investors who build the most wealth are not the ones who picked the optimal strategy on paper. They are the ones who picked something they could maintain through multiple market cycles without abandoning it when things got difficult.

Whether that means a single index fund, a globally diversified portfolio, or a managed approach with professional rebalancing, the principle remains. The gap between what markets return and what investors earn is a discipline gap, and closing it matters more than almost any allocation decision.

FAQs

What is the difference between active and passive investing?

Active investing involves a fund manager or individual making frequent decisions to try to beat a benchmark like the S&P 500. Passive investing means buying funds that track an index and holding them. Active costs more in fees and demands more decisions, while passive aims to match market returns at minimal cost.

Is it better to be an active or passive investor?

For most people, passive investing produces better long-term results. Over 90% of active large-cap funds underperform their benchmarks over 20 years according to SPIVA data. Active management can work in niche markets with information asymmetry, but identifying winning managers in advance is extremely difficult.

Is the S&P 500 active or passive?

The S&P 500 is a market index, not an investment product. Funds that track it, like Vanguard's VOO or iShares' IVV, are passive investments. An actively managed fund might use the S&P 500 as its benchmark to measure whether its stock picks are actually adding value.

Can you combine active and passive strategies?

Yes. A common approach uses passive index funds for the core of a portfolio (70-80%) and allocates a smaller portion to active strategies in segments where they may have an edge, like small-caps or emerging markets. Financial professionals sometimes call this a "core-satellite" strategy, and it can work well if the active allocation is kept proportionally small.

What is the 70 20 10 rule of investing?

The 70 20 10 rule is a budgeting framework: 70% of income to expenses, 20% to savings and investing, 10% to debt or discretionary spending. It is not strictly an investment allocation rule, though some investors adapt the proportions for portfolio construction.

Why do active fund managers underperform?

Three main forces work against them: fees create an annual headwind that the manager must overcome just to match a passive alternative, performance tends to revert to the mean making consistent outperformance statistically unlikely, and large liquid markets price information efficiently making persistent mispricings very hard to find and exploit.

Sources

- "SPIVA U.S. Scorecard Year-End 2023." S&P Dow Jones Indices. spglobal.com

- "Buffett's Bet with the Hedge Funds, Ten Years On." Berkshire Hathaway Annual Letter, 2017. berkshirehathaway.com

- "Quantitative Analysis of Investor Behavior." Dalbar Inc., 2024.

- "The Case for Low-Cost Index Fund Investing." Vanguard Research. vanguard.com

- "SPIVA Europe Scorecard Year-End 2023." S&P Dow Jones Indices. spglobal.com

Disclaimer

This article is for educational purposes only and does not constitute personalized financial advice, a recommendation to buy or sell any security, or an endorsement of any specific platform or product. All investment involves risk, including loss of principal. Past performance, including the statistics and examples cited, does not guarantee future results. Fee comparisons use hypothetical scenarios for illustration. Consult a qualified financial advisor before making investment decisions.

No items found.